Register for your free account and gain access to your "My ETFs" watch list. Located on the top panel of the Horizons ETFs website, "My ETFs" allows you to conveniently view pricing and NAV information about selected ETFs across all of your devices. All personal information is secure and will not be shared.

My ETFs

Visit your favourite ETFs and click "Add to My ETFs" to begin your watchlist.

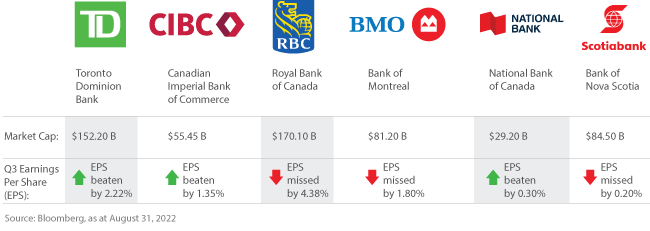

In Canada, the “Big Six” Banks – National Bank of Canada, Royal Bank of Canada, Bank of Montreal, Toronto Dominion Bank, Bank of Nova Scotia, and Canadian Imperial Bank of Commerce – are big businesses.

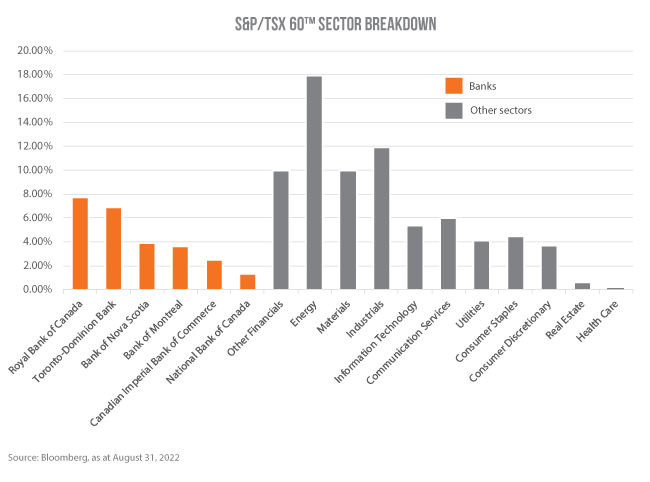

Together, Canada’s “Big Six” Banks make up nearly 25% of the total capitalization of the S&P/TSX 60 ™ benchmark, representing the country’s largest industry, both by market capitalization and revenue.

Sector Breakdown

The relative strength of the Canadian banks has proven itself throughout several market conditions:

During the 2008 Financial Crisis, the Canadian banking sector proved itself resilient, escaping “relatively unscathed”, while American and European banks teetered on the brink of collapse.

While many sectors saw their profits shrink during the COVID-19 pandemic, Canadian banks posted record profits.

Now, as the Bank of Canada struggles to tame rising inflation brought about by COVID-19 stimulus spending through interest rate hikes, Canadian banks could continue to be well-positioned to take advantage of the rising interest rate environment. However, recent disappointing Q3 earnings results from the banks could also suggest some trouble brewing.

With a potential recession on the horizon, broader economic trouble could create some vulnerability for Canadian banks. From reduced spending to growing mortgage defaults, not achieving a “soft landing” could threaten the balance sheets of Canada’s banks.

Will Canada’s “Big Six” Banks continue to be the keystone of the Canadian economy and deliver growth opportunities or could economic headwinds create a perfect storm? Let’s take a look at a few indicators that could impact the outlook for Canadian banks in the near and mid-term period:

1. Historically Rising Interest Rate Environments Can Bode Well for Canadian Banks

Historically, Canada’s banks have benefitted from rising rate environments, as it allows these financial institutions to increase the cost to borrow and access credit, achieving a higher margin on loan-based products.

In the chart below, we’ve recorded the historical performance of the Canadian “Big Six” Banks (on an equal weight basis) against the historical interest rates of the period.

As you can see, on a historical basis, there is a positive correlation between stock price returns and periods of rising interest rates. This is particularly evident during several key periods of rising interest rates: 1980 – 1982, 1993 – 1995, 2004 – 2007, and 2021 – 2022.

Annualized Return during Rising Rates Periods

BMO

CIBC

TD

RBC

NBC

Scotia

S&P/TSX Capped Composite Total Return Index (T00CAR)

1993-1995

15.98%

20.01%

17.70%

12.81%

15.67%

12.74%

14.90%

2004-2007

4.79%

6.10%

15.73%

16.85%

8.62%

15.08%

16.31%

2021-2022

19.89%

13.38%

15.08%

14.44%

16.78%

9.10%

9.99%

Whole Period 1993-2022

12.85%

12.47%

14.63%

14.70%

15.29%

13.08%

9.27%

Source: Bloomberg, as at August 31, 2022

With interest rates up already 3% in 2022 and with more hikes expected in the coming months, Canadian banks could have the potential to further pad their margins in the higher interest rate environment. At the same time, higher rates do carry risks, including the potential for greater loan defaults. Canada’s banks will need to ready themselves for those conditions by building cash reserves. Either way, the correlation between the Canadian banks’ stock price and periods of higher inflation could be one signal for investors to consider whether taking an outsized position is the right move for them.

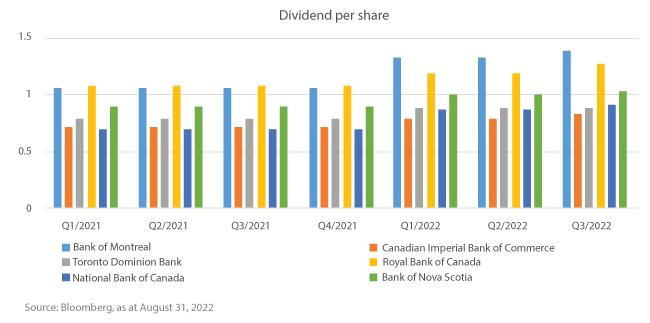

Dividend Per Share Payout (Q1 2021 – Q3 2022)

2. Could Economic Headwinds Make Canadian Banks Vulnerable?

While rising interest rates could provide greater profitability opportunities for Canadian banks, higher rates could also have negative impacts on other aspects of the Canadian economy, including a potential recession, mortgage defaults, and unemployment, which in turn, could also impact the banks’ bottom line.

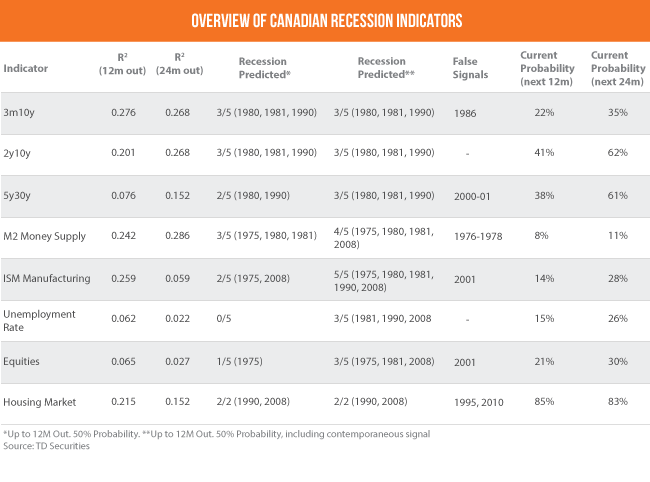

A number of analyst forecasts are predicting some level of recession in Canada in 2023. A recent TD Securities note highlighted the probability of recession based on individual indicators. Overall, TD Securities found that there is a 40% probability of a recession over the next 12 months and a 50% probability over 24 months.

What does that mean for Canada’s banks? According to RBC Capital Markets, Canadian bank earnings estimates for 2023 could fall by 16 percent on average in the case of an economic downturn. At the same time, as at August 18, 2022, RBC also notes that the Canadian banks are trading around 1.5x price-to-book value, which “effectively prices in a garden variety recession”, currently.

Average P/E over 20 years

Maximum P/E over 20 years

Date

Minimum P/E over 20 years

Date

Curent P/E

Bank of Montreal

12.20

18.74

03/23/2020

6.03

10/24/2002

9.0

Canadian Imperial Bank of Commerce

12.43

72.04

03/23/2020

5.56

02/01/2008

8.56

Toronto-Dominion Bank

13.39

38.79

02/23/2009

7.29

09/04/2002

10.41

Royal Bank of Canada

13.26

20.22

03/23/2020

8.03

03/24/2006

11.14

National Bank of Canada

11.28

20.02

12/18/2008

5.56

09/10/2008

8.90

Bank of Nova Scotia

12.41

17.73

03/23/2020

6.63

09/29/2009

8.58

Source: Bloomberg, as at August 31, 2022

As Morningstar equity analyst Eric Compton highlights, Canadian banks are sensitive to the broader macroeconomic environment and while they should be able to weather any recessionary environment, they may experience some “short-term pressure” on their stock performance.

Is that downward pressure a reason to avoid buying the Canadian banks until a recession is in the rearview mirror? Let’s take a look at how a tactically-minded investor could take advantage and potentially profit from falling valuations, or, position themselves for a potentially outsized return on a bounce back!

How Can You Trade Both Sides of the Bitcoin Opportunity?

Whether you think Canadian banks will continue to deliver strong returns or might be vulnerable to broader economic issues on the horizon, high conviction short-term traders might want to consider long and short ETFs. Leveraged and inverse leveraged Canadian Bank ETFs offer the ability to take outsized long and short positions on the equal-weight performance of Canada’s “Big Six” Banks, without the use of a margin account.

In Canada, Horizons ETFs is the only provider of leveraged and inverse leveraged ETFs, including the world’s only 2x leveraged and -2x inverse leveraged Canadian Bank ETFs, which trade on the Toronto Stock Exchange (“TSX”).

For high conviction short-term traders that think the Canadian Banks have opportunities for greater profit amid an elevated interest rate environment, they could consider the BetaPro Equal Weight Canadian Bank 2x Daily Bull ETF (TSX: HBKU), which provides two times (200%) the daily performance of the Solactive Equal Weight Canada Banks Index.

For high conviction short-term traders that think the Canadian Banks could potentially see their balance sheets and stock prices decline amid worsening economic conditions, they could consider the BetaPro Equal Weight Canadian Bank -2x Daily Bear ETF (TSX: HBKD), which provides up to two times (200%) the inverse (opposite) of the daily performance of the Solactive Equal Weight Canada Banks Index.

History shows that Canadian banks have been and continue to be a key driver of the broader Canadian stock market. Historically, betting against the banks has been a losing proposition from a return perspective, but that is not to say they are foolproof investments. Indeed, there are periods of high losses in the Canadian bank sector – most notably during the 2008/2009 financial crisis, but the Canadian banks also tend to have a higher proportion of long-term holders, unlikely to want to sell their positions in these stocks given the capital gains tax consequences. This is where a short position on the banks using an inverse ETF could be of some value, as it would effectively hedge long-term positions on Canadian banks during periods where the investor has the conviction that they could be due for substantial losses.

For traders seeking simple, non-leveraged, equal-weight long exposure to Canada’s “Big Six” Banks, they could also consider the Horizons Equal Weight Canada Banks Index ETF (TSX: HEWB).

For traders seeking exposure to Canada’s “Big Six” Banks in an equal weight portfolio, they could also consider the Horizons Equal Weight Canadian Bank Covered Call ETF (TSX: BKCC). BKCC uses a dynamic covered call strategy to help generate additional income on the portfolio.

Learn more about Horizons ETFs’ family of BetaPro ETFs

Horizons ETFs family of BetaPro ETFs offer daily leveraged (up to 2x), inverse (-1x) and inverse leveraged (up to -2x) exposure across a variety of indices, sectors, asset classes and commodities. Our suite of BetaPro ETFs are designed for investors seeking short-term, tactical trading vehicles and are comfortable managing investments with greater risk potential.